After completing her first 5km run, Annette Ball was in floods of tears at the achievement.

It was the first milestone on a journey, starting in 2019, that has seen the 56-year-old music teacher from Coventry lose more than three stone in weight and establish a new regime of strenuous exercise nearly every day of the week.

Ball’s story is the kind of inspiring tale of self-improvement that flourishes on social media feeds, but what is more unusual is the company that she credits for getting her moving: her insurer.

A points-based scheme offered by life and health insurer Vitality, which uses a wearable device to track physical activity and offers financial benefits and vouchers for progress, was instrumental to her lifestyle shift.

“The bottom line is that it is insurance, but what it has enabled me to do is get healthier,” Ball says. “It’s certainly changed how I live now.”

It is just one example of a shift that is reshaping the centuries-old insurance sector, fuelled by new technologies and real-time data that insurers are increasingly gathering on their customers.

Vitality calls it “shared-value insurance”, others call it “active insurance”, but the core idea is the same — focusing more and more on preventing and mitigating claims. By working with consumers and businesses to change behaviour and reduce their risks, insurers hope to limit the likelihood and severity of payouts.

Prevention has been an element of the insurance industry for centuries. In the aftermath of the Great Fire of London, the property insurers of the 17th century operated their own emergency services, as they sought to protect themselves as well as their clients. From burglar alarms on houses to wheel locks in cars, insurers have long urged clients to take more measures to avoid thefts that would result in claims.

But smarter and widely available technology means insurers can now intervene earlier and in a greater variety of ways — an accelerating process that is starting to change large parts of the industry.

Companies have been experimenting with using these types of tools in health insurance for more than a decade. They are now increasingly prominent in areas ranging from floods to cyber attacks. Cyber insurance provider CFC has called its support services “digital fire trucks”.

“We’re investing heavily into risk prevention . . . in order to help turn insurance from just paying out to essentially helping people understand their risk and reduce their risk,” says Julian Teicke, co-founder of insurtech wefox. The company raised $400mn from investors earlier this month in its latest funding round and has recently established a research team in Paris to drive its prevention efforts.

The growing focus on prevention has prompted some industry leaders to question what the insurance business will look like in the future. In particular, some question whether the provision of insurance coverage — the financial risk taken by the provider, which has been the backbone of the industry — will end up as just one element in a wider package of services.

“If prevention becomes really something mass market, the insurance product will be a smaller component [in] a broader suite of services,” said Raphaël Vullierme, chief executive of home insurtech Luko, earlier this year.

The winners, he predicted, would be technology-focused groups used to building those services.

Growing bill

Prevention is presented by insurers as a vital tool in dealing with the growing bill from threats such as the obesity crisis, cyber assaults and extreme weather.

For life and health insurers, the aim is to encourage fitter, longer-living customers; for cyber insurers, it is to ensure fewer cyber attacks break through clients’ defences; for motor insurers, safer drivers; for home insurers, it means reducing damage from floods, and catching leaks early.

Customers are incentivised by the promise of lower insurance premiums if they reduce their risks, and companies’ profit margins should be boosted if the fall in claims outweighs those discounts.

Zurich, one of Europe’s largest insurance companies, established a resilience services unit last year with 750 risk engineers working across 40 countries to help companies assess and mitigate their risks.

“We want to keep customers in business and we want to reduce [their] cost of risk,” says Sierra Signorelli, head of commercial insurance at Zurich. The intensifying frequency and severity of storms is a key driver of take-up of resilience measures among companies, she adds.

One of Zurich’s clients is automaker Audi, whose Neckarsulm factory in south-western Germany was hit by the torrential rain storms that hammered Europe in 2016, sending mud and water pouring into the plant, damaging equipment and halting production.

Audi then worked with Zurich’s risk engineers as well as local officials, the emergency services and other stakeholders to strengthen the plant’s defences and those of the surrounding area, including installing new retention basins.

When heavy rainfall hit last year, the factory was ready. Alerted by an early warning system, workers teamed up with emergency services to inflate long water-filled barriers around the facility. Thanks to the countermeasures, the final repair bill was lighter and production did not have to stop.

The cyber insurance market is increasingly a mixture of protection and cover: providers work with companies to patch holes in their digital defences, put in place extra security measures and offer emergency services to restore systems and recover data after attacks.

Cyber insurer Coalition is one of a growing number of companies in this segment of the market and places as much attention on its security services as its insurance policies.

“We look at our customers as if we were playing offence. We are looking for those nails that are sticking out,” says its chief executive Joshua Motta, a former CIA analyst.

Coalition says it scans more than 5bn IP addresses 400 times a month for vulnerabilities. That might be malware in a client’s system, or unpatched software that is vulnerable to hackers.

Some insurers now demand that companies must have basic protections such as multi-factor authentication in order to receive cover, as the sector responds to the surge in ransomware attacks.

Smarter tech

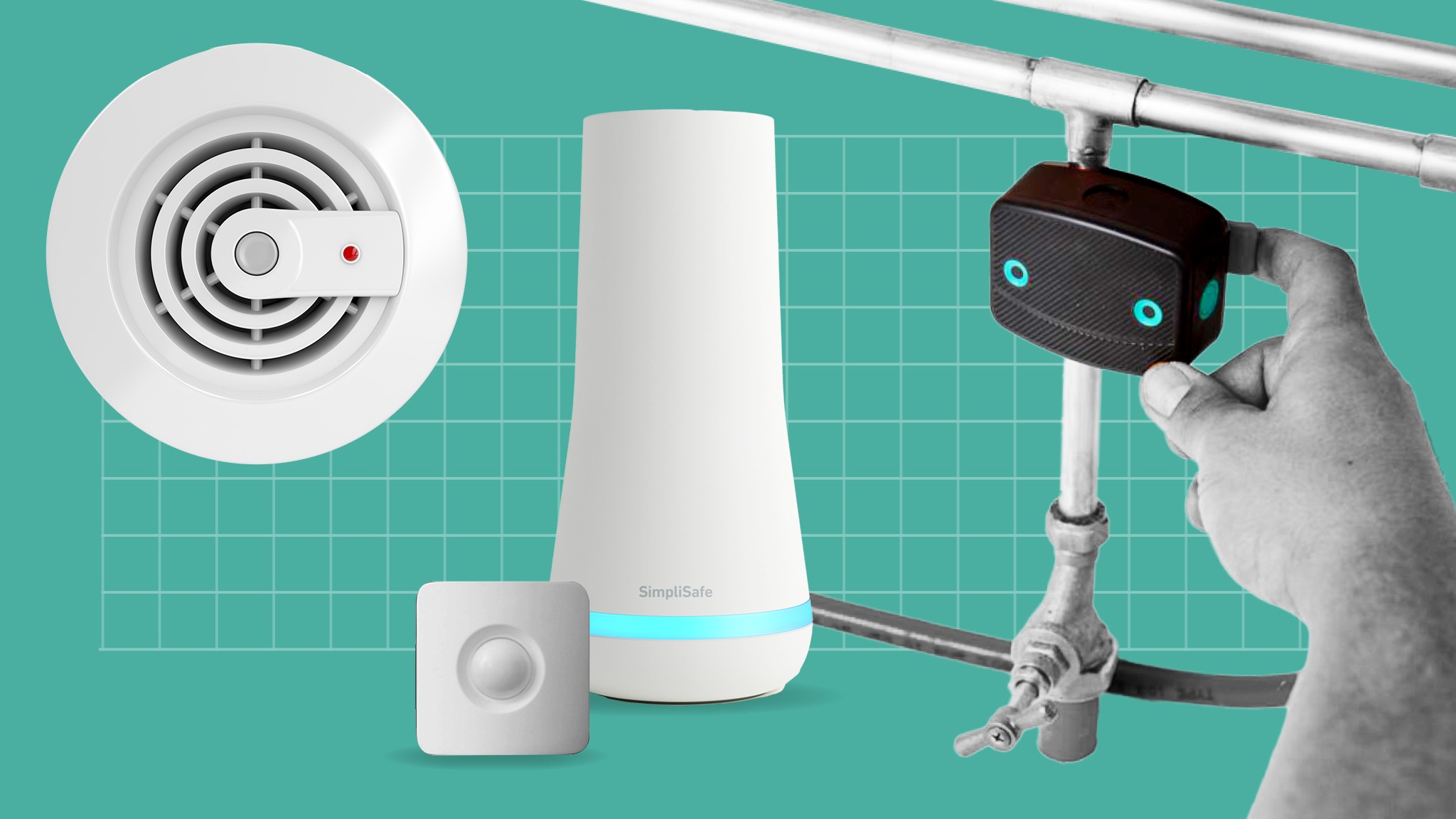

Home insurance is another frontier for prevention efforts. “The best claims experience is avoiding the claim entirely,” says Rick McCathron, chief executive at New York-listed home insurer Hippo, which supplies its customers with a range of detection systems including leak sensors, smoke alarms and motion detectors to try and stave off claims. Those who use the system can get a discount on their insurance — but only if they keep the system activated.

This makes for a fundamentally different business, argues McCathron. “We’re not a home insurance company,” he says. “We are a home protection company.” Last year, it announced a partnership model with US homebuilders to install automatic shut-off valves in new-builds that it said would “meaningfully” reduce insurance costs.

Insurers across the globe are investing in leak-detection systems to stem one of the most common sources of home insurance claims. Ondo, a London-listed provider specialising in this area of work, estimates its technology reduces water-damage claims by 70 per cent: equivalent to about £9bn of the industry’s annual water-leak payouts across the US and UK.

Home insurance

Big insurers and start-ups are seizing on leak detection and prevention technologies as they seek to choke off one of the major sources of home insurance claims: water leaks. Some offer them alongside other smart tools like connected motion sensors and smoke detectors to combat other big threats.

Ondo announced last week that Admiral, the FTSE 100 insurer with more than 1mn home insurance customers in the UK, had agreed to provide its technology to 20,000 policyholders in a pilot that could lead to a wider rollout.

Claims can also lead to better prevention by exposing blind spots and bring about solutions. Flood Re, the UK’s reinsurance scheme for flood risk, earlier this year launched a “build back better” scheme in partnership with insurers.

Customers with such policies who make a flood claim can receive up to £10,000 to make their home more resilient, such as installing flood doors and tile floors and moving electrical sockets higher.

Israel-based GeoX uses aerial imagery and other data to build a 3D image of a property that gauges risks such as roof condition, pointing customers towards preventive measures.

‘Data harvesting’

Motor insurtechs have developed a range of innovations to try and stave off claims. The use of real-time data in underwriting models has allowed start-ups such as the UK’s Zego and New York-listed Root, to reward people for safe driving, in the latest iteration of pay-how-you-drive-type policies. Increasingly, executives are talking about how they can provide feedback to customers and influence their behaviour.

By Miles, a UK car insurtech, has been developing processes to contact customers in the event of a weather warning, encouraging them to move their vehicle to high ground, says chief executive James Blackham.

In another recent episode, a customer in Sheffield in England managed to locate their stolen car to a local KFC car park using By Mile’s car-tracking tech.

In such cases, some customers end up not filing a claim at all, says Blackham. “Most people get the car back and [compared with] paying their excess, it doesn’t make any sense. It might need a bit of a vacuum round inside, or something like that.”

Life and health insurance offers perhaps the greatest hopes for such a proactive approach to risk, powered by the growing use of wearables as well as more sophisticated real-time underwriting models.

Insurers talk excitedly about the potential to use genetic data to manage health problems years in advance, though use of such data is highly controversial and usually tightly regulated.

Car insurance

A flurry of start-ups have emerged in recent years promising customers lower premiums for safer driving, using phone apps to gather behavioural data and try and influence customers. Bigger insurers, which have used telematics to offer pay-how-you-drive policies for more than a decade, have also poured investment into technologies that provide personalised feedback and tips based on a customer’s driving style.

China’s Ping An, one of the largest insurance groups by market value, offers health cover that gives those diagnosed with type-2 diabetes a diet and exercise plan to reduce their risk of complications. Compliance can mean an insurance discount.

But some industry observers worry about where the closer relationship between insurers and their customers will lead.

“No one ever talks about the negative side,” says Duncan Minty, an independent consultant on ethics in insurance. “Because risks do happen, there will be cases where things can go better for the consumer and cases where they go worse.”

Insurers argue that getting a more specific picture of an individual customer’s risks could actually increase the amount of people who can get insurance — including those they had previously been unwilling to cover.

But Minty warns that wearables and real-time technology could lead to “data harvesting” — gaining granular and constantly updating detail about customers’ behaviour — that might be less about loss prevention and more about generating a closer risk profile of customers that is to the insurer’s advantage.

There is a “real chance”, he says, that customers might either be not offered a premium, or be offered one that is so high that it becomes unaffordable. Minty worries that insurers will ultimately use the data to create policy terms that demand compliance as a condition of remaining covered.

Death of coverage

There is potentially a self-defeating logic to prevention from the industry’s perspective. Claims are the lifeblood of insurance companies, the basis that allows companies to charge premiums, so meaningfully cutting them could reduce future revenues.

But many claims cannot be prevented. Andrew Scott, who heads up research and development at the UK arm of insurer Vitality, divides risks into modifiable and non-modifiable ones.

That also provides an answer to the fairness question, he says. “We argue that it is fairer for people to pay for the unique risks that they present, if they are able to change those risks,” Scott adds.

Life insurance

Life and health insurers have been early adopters of using wearable and app technology to incentivise their customers to get healthier, with the promise of lower insurance costs and other benefits. Reducing the risk of major illnesses can prevent or reduce claims, and longer-living life insurance customers means accruing more insurance premiums on a typical policy.

The reduced claims bill that comes from keeping customers healthier than they would be otherwise is “counterbalanced”, he adds, by the payouts for more advanced diagnosis and treatments.

Some industry experts think the pivot to more prevention and protection will reduce the primacy of the insurance coverage within the services that companies can offer.

That might put insurers in greater competition with other tech and services groups. Almost half of the people cyber insurer Coalition hires are software engineers. Ondo, which proclaimed itself the first UK insurtech to list after joining the London stock market earlier this year, was spun out of Home Serve, which provides emergency repair for items such as boilers.

Whether some of the new technologies do indeed lead to a lower loss ratio, a key profitability measure which shows claims as a proportion of premiums, remains an open question.

Some of the highest profile insurtechs, such as Root, have suffered big underwriting losses as they try and grow their businesses — partially due to the uptick in claims that comes with new customers. This obscures the view of whether the newer technologies and behavioural nudges are helping them to price risks more effectively.

Another more immediate prize could be a deeper relationship with the customer, who might not so easily jump ship to another insurer.

“I think I’ve got an awful lot out of it,” says Ball of her programme. “It’s certainly changed how I live now.”